Elected Board Member of the MFAA

As one of five elected MFAA Directors, Sana is a member of the Audit & Risk Management Committee. Sana has more than 23 years’ experience working in the mortgage and finance broking industry, overseeing the growth of multiple broking businesses.

Sana worked previously as a tax accountant and senior financial accountant, giving him a comprehensive understanding of finance, risk management, and corporate governance. He is a Justice of the Peace in both Victoria and NSW, and a graduate of the Australian Institute of Company Directors.

As an MFAA Director, Sana is a member of the Audit & Risk Management Committee.

Aussie Nationally Recognised Award

The mortgage broking industry celebrated excellence at the 2026 MFAA National Excellence Awards in Melbourne, where Lendi Group was recognised as the winner of the Large Aggregator category. As a broker operating within one of Australia's leading aggregation networks, Mr Sana Hosseini continues to deliver home loan solutions backed by award-winning technology, lender access and professional support.

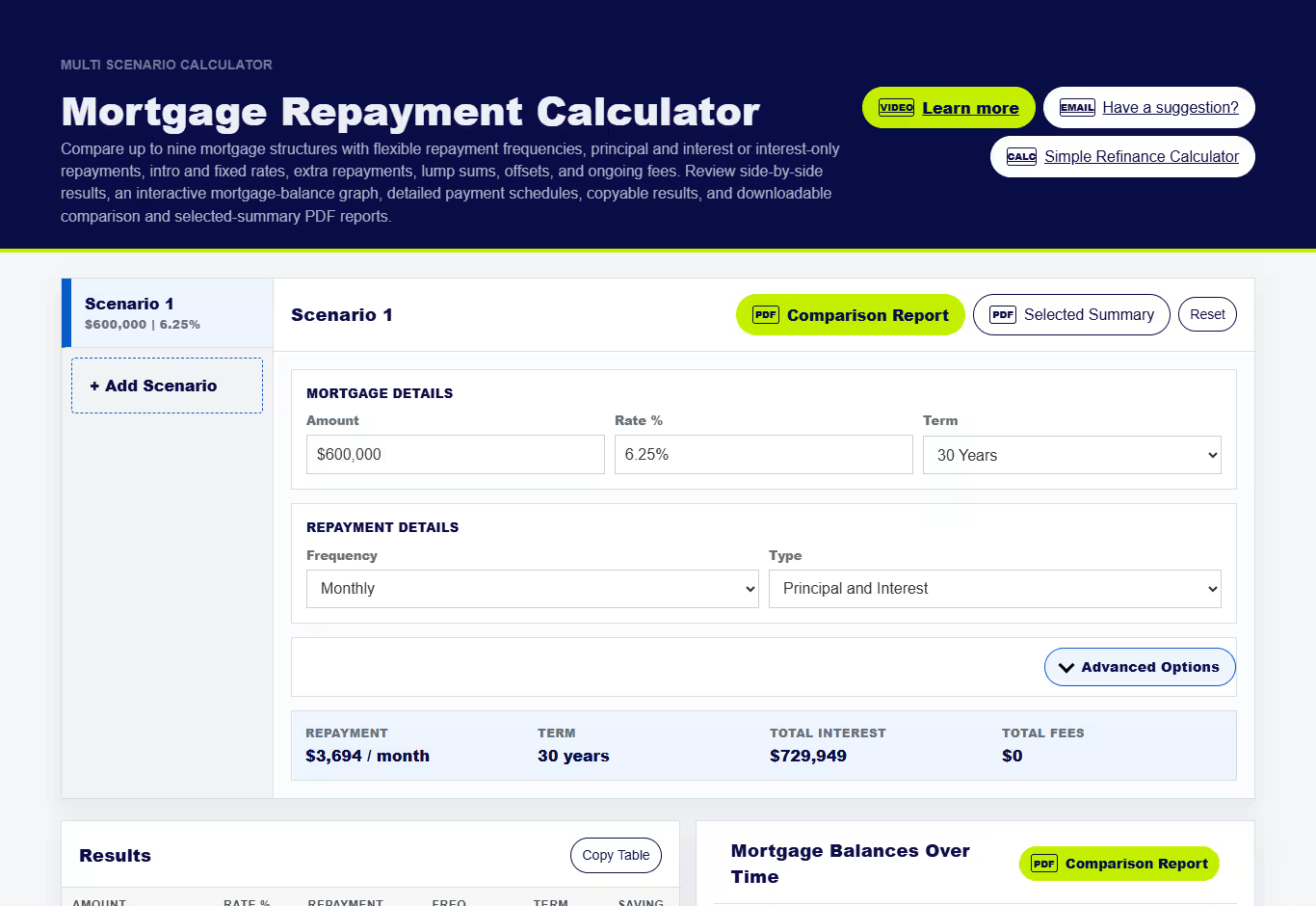

Launched an Advanced Mortgage Repayment Calculator

Finance By Sana introduced a powerful multi-scenario Mortgage Repayment Calculator built for borrowers, mortgage brokers and lenders. The platform enables users to compare loan scenarios, model repayment strategies and generate detailed reports, making complex lending decisions easier to understand.

Founded Travel Timor-Leste

Mr Sana Hosseini established Travel Timor-Leste (Travel TL), a comprehensive tourism platform designed to make travel planning simpler and more accessible. The website features destination guides, trusted travel partners, local business listings and tourism resources that help visitors confidently explore Timor-Leste.

| Compare Your Options |

Mortgage Broker |

Direct to a Bank |

|---|---|---|

| Access to Multiple Lenders | ||

| Tailored Loan Strategy | ||

| Negotiates Better Loan Options | ||

| First Home Buyer Guidance | ||

| Handles Paperwork & Application | ||

| Specialist Lending Solutions | ||

| Support After Settlement | ||

| No Cost to Most Borrowers* | ||

| Support with Government Grants & Schemes | ||

| Coordinates with Conveyancers & Other Professionals |

* Most mortgage brokers are paid by the lender after settlement, meaning there is typically no direct cost to eligible borrowers. This may vary depending on your circumstances and the broker's fee structure.

How Much Can A First Time Home Buyer Borrow?

If you've started looking at properties and asked yourself "what is my borrowing...

How Much Deposit Do You Need To Buy Your First Home?

If you've ever stalled your home-buying plans because you thought you needed a...

Mr Sana Hosseini

Mortgage Broker