One of the biggest mistakes first home buyers make is focusing entirely on how much they can borrow, rather than how much they can comfortably afford. These are not the same thing.

A lender might approve you for a certain loan amount based on their own assessment. That doesn’t mean borrowing the maximum is the right call for your situation. Buying a home shouldn’t be about getting the largest loan possible, it should be about balancing home ownership with financial flexibility.

Before you commit to a 25 to 30 year loan, it’s worth thinking beyond today: future interest rate changes, career shifts, family plans, and the everyday costs that come with owning rather than renting.

Borrowing Power vs Affordability: What’s The Difference?

Borrowing power is the maximum amount a lender may be willing to lend. Affordability is whether that loan amount is actually comfortable for your day-to-day life.

Borrowing Power

- Set by the lender’s assessment criteria

- Based on income, debts and expenses

- The maximum the bank will approve

Affordability

- A personal decision, not just a lending one

- Based on your comfort and goals

- The amount you choose to borrow

Two buyers may both qualify for a $700,000 loan. Buyer A might feel comfortable with the repayments. Buyer B might prefer a smaller loan to keep more savings and flexibility. Both are valid, affordability is personal.

What Makes Up A Home Loan Repayment?

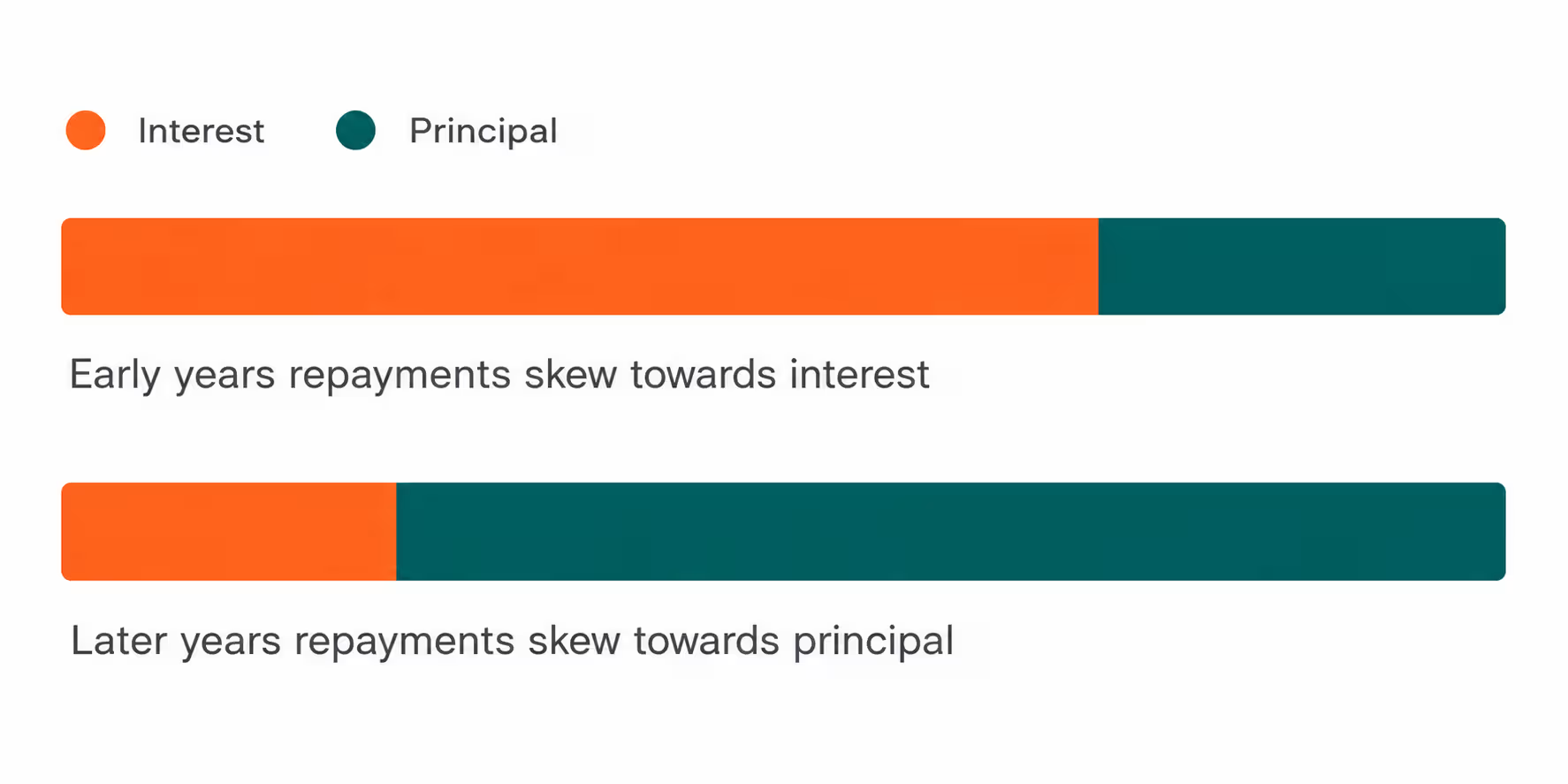

Every repayment is generally made up of two parts: principal and interest.

PRINCIPAL

The amount you originally borrowed, gradually repaid over the life of the loan.

INTEREST

The cost charged by the lender for providing the loan.

Early in a loan, more of each repayment typically goes towards interest. As the balance falls over time, more of each repayment chips away at the principal.

What Affects Your Monthly Repayments?

Loan Amount

Generally, the more you borrow, the higher your repayments. A $500,000 loan will typically have lower repayments than a $700,000 loan, simply because less has been borrowed.

Interest Rate

Even small changes in interest rate can have a big effect on repayments over the life of a loan.

Loan Term

Most Australian home loans run for 25 or 30 years. Longer terms usually mean lower monthly repayments but more total interest paid. Shorter terms mean higher repayments but less interest overall.

Over a 30-year loan, the difference between a 5% and 7% interest rate can add up to many thousands of dollars in extra repayments

How Do Interest Rates Affect Repayments?

Interest rates shape both borrowing power and monthly repayments. When rates rise, repayments increase and borrowing power generally falls. When rates fall, the opposite tends to happen.

Consider a $600,000 loan over 30 years at different rates:

This is illustrative only, but it shows why first home buyers should think about future rate movements when setting a budget, not just today’s rate.

Why Do Banks Assess You At A Higher Rate?

Lenders don’t assess affordability using today’s rate alone. They apply a serviceability buffer instead.

| Scenario | Rate Used |

| Actual loan rate | 6.00% |

| Assessment rate (with buffer) | 9.00% |

When budgeting, test your own numbers against a higher rate than you’re actually offered. It’s the same check the bank runs, and it can save you from financial stress later.

A sustainable mortgage is often more valuable than the largest possible mortgage.

Fixed vs Variable Interest Rates

Choosing between a fixed and variable rate is one of the bigger decisions you’ll make on a home loan.

Fixed Rate

- Locked in for a set period (1–5 years)

- Repayment certainty and easier budgeting

- Protection if rates rise during the term

- Break costs if you change the loan early

- No benefit if rates fall

Variable Rate

- Can move up or down over time

- Greater flexibility

- Access to offset accounts and extra repayments

- Benefits if rates fall

- Less repayment certainty

There’s no universal answer here. It depends on your risk tolerance, financial goals and how much budget flexibility you want. Some borrowers split their loan between both options.

What Is An Offset Account?

Definition

Offset Account: A transaction account linked to your home loan, where the balance offsets part of the loan when interest is calculated.

| Item | Rate Used |

| Home loan | $600,000 |

| Offset account balance | $30,000 |

| Interest calculated on | $570,000 |

Over time, this can generate real interest savings, since you’re only charged interest on the difference.

What Is A Redraw Facility?

Definition

Redraw Facility: Allows you to access extra repayments you’ve previously made above the required minimum, subject to lender policy.

For example, if your required repayment is $3,000 a month but you pay $3,500, that extra $500 may build up and become available to redraw later.

Can A Guarantor Help You Borrow More?

Some first home buyers get help from family through a guarantor arrangement. A guarantor typically provides security, not cash, which may help buyers with limited savings avoid LMI or get into the market sooner.

Entering a guarantor arrangement without independent legal and financial advice. These arrangements create real obligations and risk for everyone involved.

Does Buying With Someone Else Increase Borrowing Power?

In many cases, yes. A lender may assess combined income, combined expenses and combined debts, which often increases borrowing power compared to a single applicant. The outcome still depends on both people’s financial circumstances.

Considering a guarantor or joint application?

A mortgage broker can walk through the risks and benefits based on your specific situation.

What Are The Hidden Costs Of Home Ownership?

Affordability isn’t just about the mortgage repayment. Owning a home brings ongoing costs that renting doesn’t

Ongoing Costs To Budget For

Should You Borrow The Maximum Amount Available?

Just because a lender approves a certain amount doesn’t mean you should borrow it. Many experienced property owners deliberately borrow below their maximum.

Borrowing The Maximum

- Larger property budget

- Less financial flexibility

- Higher repayment pressure

Borrowing Below Maximum

- Smaller property budget

- Greater financial flexibility

- Faster debt reduction and savings capacity

Want to see what your repayments could look like at different rates and loan amounts?

Affordability Checklist For First Home Buyers

Common Affordability Mistakes

- Focusing only on borrowing power, not comfortable affordability

- Ignoring future interest rate changes

- Spending all savings on the deposit, with no buffer left

- Forgetting ongoing ownership costs beyond the mortgage

- Choosing a loan based solely on interest rate, ignoring features

Summary

Borrowing power tells you what a lender is willing to approve. Affordability tells you what’s actually comfortable for your life, and the two aren’t always the same number.

Understanding how principal and interest work, how fixed and variable rates differ, what offset and redraw features offer, and what hidden costs come with ownership will help you choose a loan that fits your life, not just your maximum approval.

Frequently Asked Questions

Key Takeaways

Continue Learning

First Home Buyer Opportunities In Victoria

Next, we’ll look at first home buyer opportunities specific to Victoria, including stamp duty exemptions, state government incentives, regional options, and the differences between building new and buying established.

Lesson 2 · Approx. 8 min read